In partnership with

Welcome to the Skeptical Investor Newsletter. A frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

The Weekly 3 in News:

First-time homebuyers today average 38 years old, which means they are as close to getting their first Social Security check as to when they graduated high school (24 years vs 20 years). Holy hell! (Lambert).

How old are repeat homebuyers today vs the past?

42 years old → The median age of repeat U.S. homebuyers in 1991.

61 years old → The median age of repeat U.S. homebuyers in 2024 (Lambert).

Today’s Interest Rate: 7.05%

(Unchanged from this time last week, 30-yr mortgage)

Today, I want to dig further into what the Treasury Dept is attempting to do on mortgage rates. In my view, this is going underreported / under-analyzed. If you are in real estate, this effort is a big deal.

This is a follow-up on last week’s government spending/DOGE article, which is on pace for 100,000 views! (My most popular new letter yet). If you didn’t get a chance, it’s still available for free here.

Let’s get into it.

Mortgage Rates: The state of play

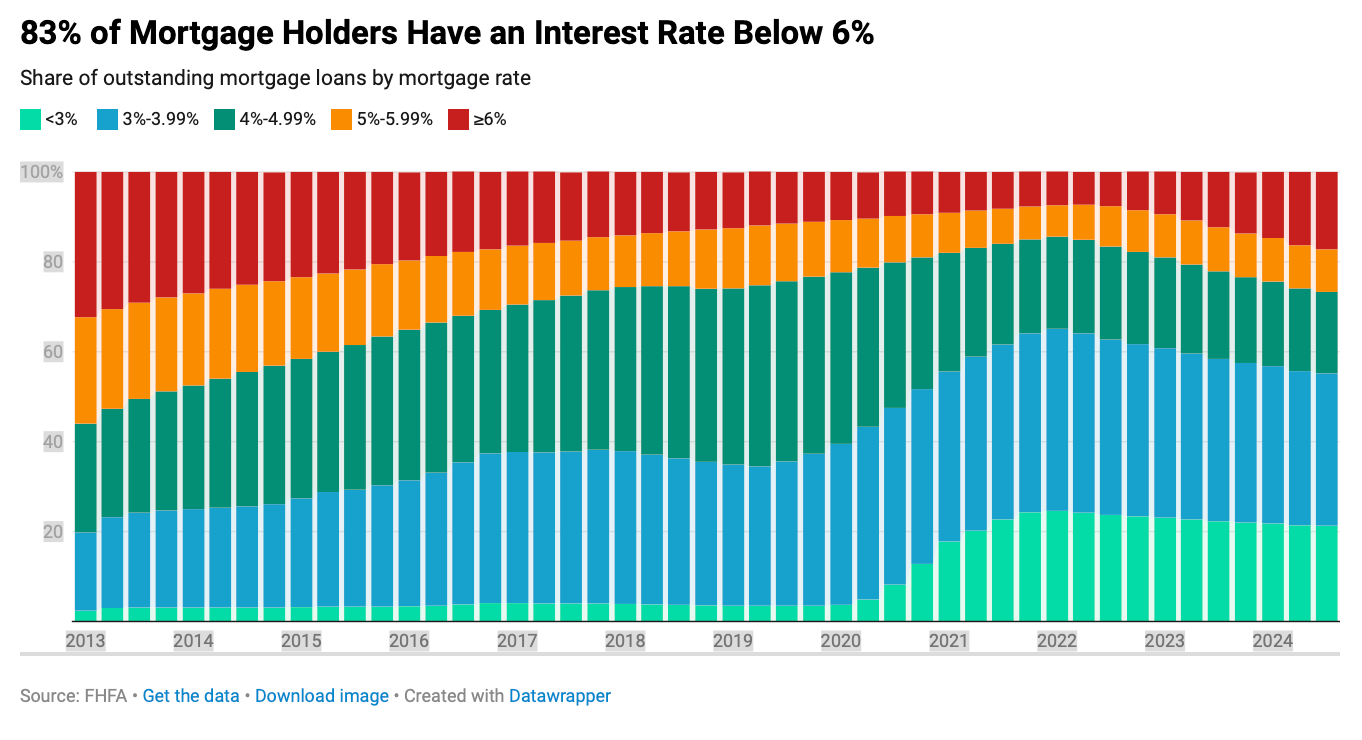

Today, mortgage rates are 7.05%, yet 82.8% of homeowners with a mortgage have an interest rate below 6% and 55% are below 4%. This makes selling a home, only to buy another, quite painful. Homeowners are still handcuffed to their home. This continues to depress real estate activity.

However, transactions are still happening, albeit far below the historical activity levels. Existing home sales in December 2024 was the lowest level in nearly 30 years (4.06 million annualized), while the median price reached a record high of $407,500.

The Fed Has No Good Reason to Cut Rates

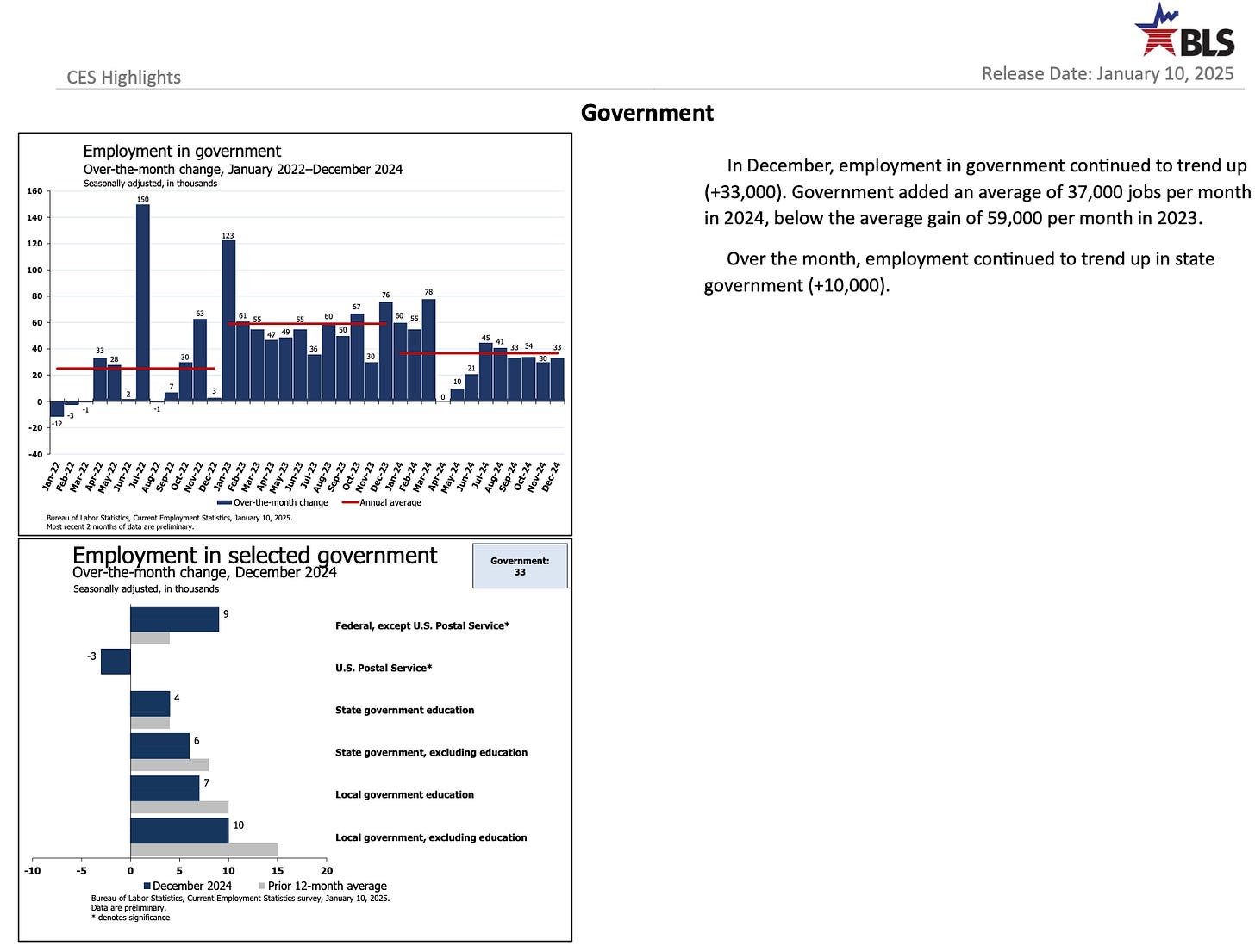

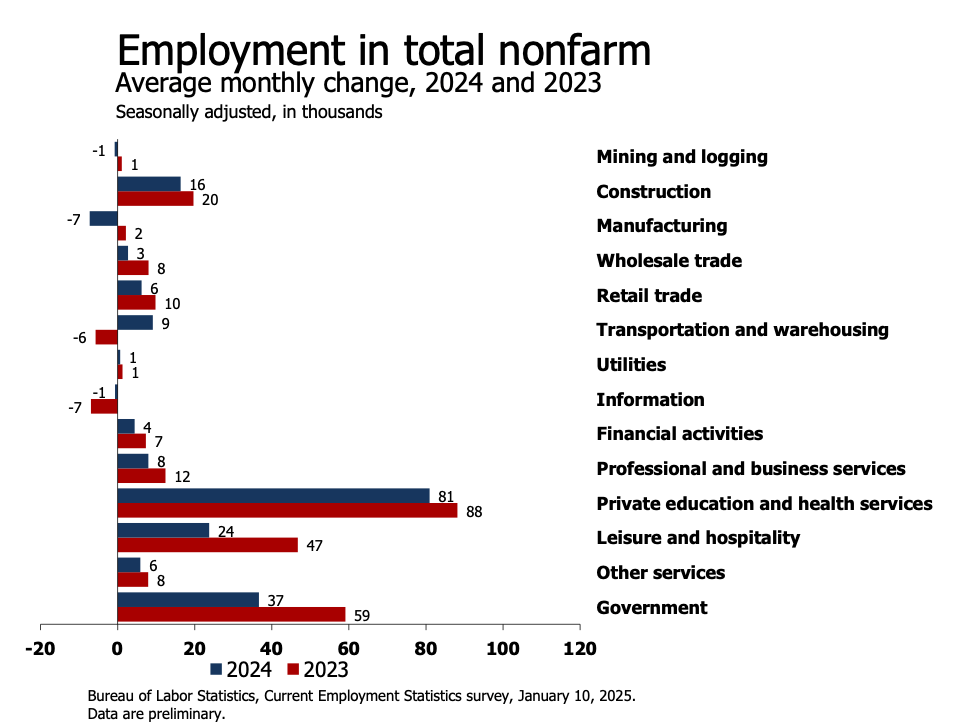

The Federal Reserve has largely achieved its dual mandate of maximum employment and stable prices. But there is no good excuse for the Fed to cut interest rates, at this time. The Fed needs the labor market to break or slow more significantly. Although it is softening. One glaring example: we had an explosion in government hiring the last 2 years. This will definitely not happen again in the current political climate.

Wild Fact: did you know the Federal Government added 37,000 employees per month in 2024? And that this was down from 2023, when they added ~60,000 per month?

Holy hell.

In fact government, was the second fastest growing employment sector.

Wow.

But I digress…

Labor Market is Still Strong

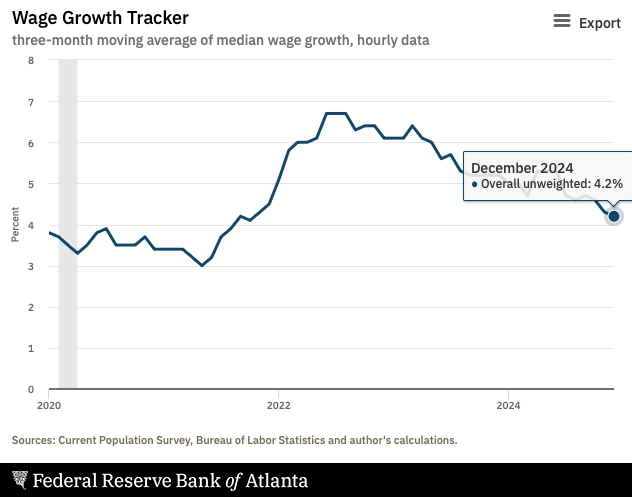

The labor market is still quite robust, unemployment is staying low at 4% and wage growth is still a solid 4.2%, growing much faster than current 2.6% PCE inflation.

These are not conditions in which the Fed will cut rates.

So with a strong economy (yay!) and great jobs numbers (also yay!) mortgage rates are poised to stay elevated for much longer (boooooooo!).

This has caught the attention of the new folks over there at the US Treasury….

Do you hate email? I do.

Well, they finally did it, an AI email assistant. Let AI do email for you. Read, filter, respond, notate, a back massage for crooked neck (ok not that, yet)…it’s Fryer AI.

Begin your day with emails neatly organized, replies crafted to match your tone, and crisp notes from every meeting….Holy hell they did it. It’s superhuman and frankly amazing! Links to your Gmail or other email service.

Plus, you get a free 7-day trial from us at the Skeptical Investor.

Support our pirate ship by clicking the ad below, each click promotes our newsletter! 👇

Sell Smarter with Fyxer AI

For busy property specialists, admin tasks can pile up fast.

Enter Fyxer, your AI Executive Assistant:

Emails organized and ready for your day.

Personalized replies crafted to match your tone.

Detailed notes from every meeting.

Spend less time on admin, more time on deals.

Try a 7-Day Free Trial—no credit card required! Integrates seamlessly with Gmail and Outlook.

US Treasury Dept: Mortgage Rates are in the Crosshairs

The Fed is not likely to cut more than 2 times in 2025, if that. Bank of America and Morgan Stanley say there will be one, or possibly no, rate cuts this year. And most financial institutions agree: Fannie Mae, Wells Fargo, Mortgage Bankers all think mortgage rates will end up around 6.5% in 2025.

So if you’re waiting for the Fed to come to the rescue, it’s going to be a long wait.

It appears that the incoming Treasury Secretary Scott Bessent recognizes this and will be concentrating on the bond market and inflation, saying:

“We are not focused on whether the fed is goin to cut [or] not cut, what we are focusing on is lowering rates…the 10yr is the important price to focus on…it’s mortgages, it’s long term capital formation…I think the 10-yr will naturally come down… and on top of it, what if we do get some big savings from the DOGE program?”

This is positive for a variety of reasons, particularly since the President has said that he may want to try to influence the Fed’s interest rate decisions, or even have direct control over them. He has been quite critical of Jerome Powell personally. The Federal Reserve has been an independent organization, insulating it from political pressures and Fed members cannot be fired without cause.

Bessent has released an economic plan, which he formulated last year and pitched to the President during the campaign: The 3-3-3 Plan (this plan was reported as a key reason the President chose him).

What is Bessent’s 3-3-3 Plan?

‘Modestly’ grow the Economy - Achieve economic growth of 3% (Q4 was 2.3%, but 2024 was close to 3%) so deficits matter less and revenues grow,

More Energy - Increase oil (and also natural gas) production by 3 million barrels a day to put downward pressure on the input costs for goods and services, as well as fuel prices for the consumer, and

Cut Spending - Reduce the budget deficit to 3% of GDP (currently 6.3%).

Essentially, Bessent’s goal is to put downward pressure on inflation, while growing the economy, so the deficits we do have, matter less. And while the plan has received much criticism for it’s potential tactics and lofty goals, the Administration is plowing ahead.

Counterpoint: Economist and Former National Economic Council Director under Obama, Larry Summers, believes these spending cuts will not be enough to quell inflation, calling our current economic state the, “riskiest period for inflation policy since the early Biden Administration….even without tariffs, immigration restrictions, deficit bloat and attacks on the Fed there would be serious grounds for inflation worry.” He also does not think Bessent will be successful in reducing 10-yr interest rates.

Consider Becoming a Paid Subscriber!

Paid subscribers get the best stuff, including a one-on-one call with me personally. Paid Subs get the best stuff. So make sure to take advantage.

Cutting Spending and the DOGE Effort

Number #3 above seems to be where the most action is today, specifically with the DOGE team.

What is DOGE again? It’s the Department of Government Efficiency (DOGE), was formally established by executive order on January 20. Its aim is to: “[cut spending, reduce regulation, restructure federal agencies and enhance government efficiency.]” The initiative, despite its name, is not a department and it automatically shuts down early next year. The effort works through the Treasury and the Office of Management and Budget, the budgetary arms of the White House. It is headed by Elon Musk, who is now an official “special employee” and advisor to the President.

In a recent Bloomberg interview, Bessent emphasized how serious he is about the need for spending cuts and explained his support of the DOGE effort, saying, “I believe that this DOGE program is one of the most important audits to government we have ever seen.” In the interview, he does acknowledge that past efforts have failed, such as the Grace Commission in the Regan years, but insists that this time is different.

DOGE’s reception as been a tale of two cities, one side hates it and the other side is extremely excited. I’m not going to pass judgment or wade into the politics here. But it has the full-throated support of the US Treasury, which has operational control. Speaking in the same interview, Bessent said of DOGE, “the Treasury Department is in control and that there is “no tinkering with the system.” “The DOGE team is read-only. They can make no changes. It is an operational program to suggest improvements.”

So all the media reports of what DOGE is “doing” appears to be announcements of what the US Treasury is actually acting on, with their support. Again, staying apolitical, I found this nuance very important.

Why we care: This matters for us investors. The bond market won’t look positively on an effort that is not effective, serious and successful. It was important for the Secretary to make this clarification so that, if true, the markets react rationally.

Lowering Energy Prices and Mortgage Rates

Speaking in the same interview, Bessent made his case for lowering energy prices as a critical part of their war on inflation, saying, “The bond market is recognizing that energy prices will be lower and we can have non-inflationary growth.... We cut the [federal govt] spending, we cut the size of government we get more efficiency in government. And we’re going to go into a good interest-rate cycle.”

Bessent is attempting to put downward pressure on the energy input costs for goods and services, as well as fuel prices for the consumer, all in an effort to coax disinflation.

In other words, Bessent is clearly focused on bringing down interest rates at the long end of the yield curve, which in turn will mean mortgage rates do the same.

My Skeptical Take:

I am impressed at the vigor behind the spending cut effort, but will it be enough?

Again, I am passing no judgment on what to cut or why. It’s happening and IF the Administration is successful, it will have broad market effects. It’s important to discuss what these effects may be, so we, as investors, can appropriately posture.

Remember, we pay for government deficit spending one way or another, especially those who do not own real assets, like stocks, bonds, art, classic cars… and of course, real estate.

Inflation = taxation, in different form.

But don’t just take my word for it, here are a few American leaders who said the same:

Milton Friedman - "Inflation is taxation without legislation". Friedman also called inflation a "hidden tax".

Ronald Reagan - "Inflation is a tax. In fact, inflation is the cruelest of taxes because poor people tend to pay it".

John Beckley - "Inflation is a form of hidden taxation that is almost impossible to measure".

Thomas Sowell - "One of the biggest taxes is one that is not even called a tax — inflation".

Warren Buffett - "The arithmetic makes it plain that inflation is a far more devastating tax than anything that has been enacted by our legislature".

But the White House likely won’t be able to totally go it all alone. So far the DOGE effort has been successful in essentially shaming Congress and previous Administrations for wasteful spending efforts (emphasis on multiple previous Administrations for squandering our tax dollars), and while salacious and sometimes comical, that won’t be enough. Congress will likely have to act on a larger Budget Reconciliation package this Summer/Fall to reduce the deficit more meaningfully and long term. This is how the massive “Inflation Reduction Act” was passed in the last Administration and how “ObamaCare” was passed during his term. The Reconciliation process only requires a majority vote in the Senate to pass, which is why it’s a favorite legislative tool of Administrations past when they have a majority in both branches of government.

Side note: Wouldn’t it be nice if both parties could just come together to this and that it wouldn’t take 100 years? Nobody really wants inflation or wasteful spending or fraud, right? Figure it out folks!

But I digress…

Bessent knows the bond market is worried that re-inflation could occur if the economy runs at a robust 3% (his first goal above). And he also knows the Fed does not control the long end of the yield curve, ie the 10-yr treasury. The bond market is in control there, and bond market vigilantes are fighting the Fed. So even if the Fed does cut rates again, until inflation is totally under control, it won’t matter. (Remember mortgage rates track the 10-yr, not the Federal Reserve’s Fed Funds Rate).

So if you are keeping track: higher deficit spending = higher interest rates, which is why they are targeting spending so aggressively.

Will our elected leaders be able to cut spending and get deficits under control?

Perhaps, but this effort has to be serious.

How serious? Deficits should be 3% of GDP or less, absent an emergency, says former Chair of the Council of Economic Advisers under Obama, Jason Furman, who said “I'm comfortable with 3% GDP deficits… I like the higher cap on domestic spending but still have a naive belief in paying for things so as not to dig the hole any deeper.”

Secretary Bessent….Wait… did we just find something both sides can agree on?!

Bingo.

So let’s come together. Our government leaders need to find ~$500 billion/yr minimum in real cuts.

And no fuzzy budget gymnastics folks.

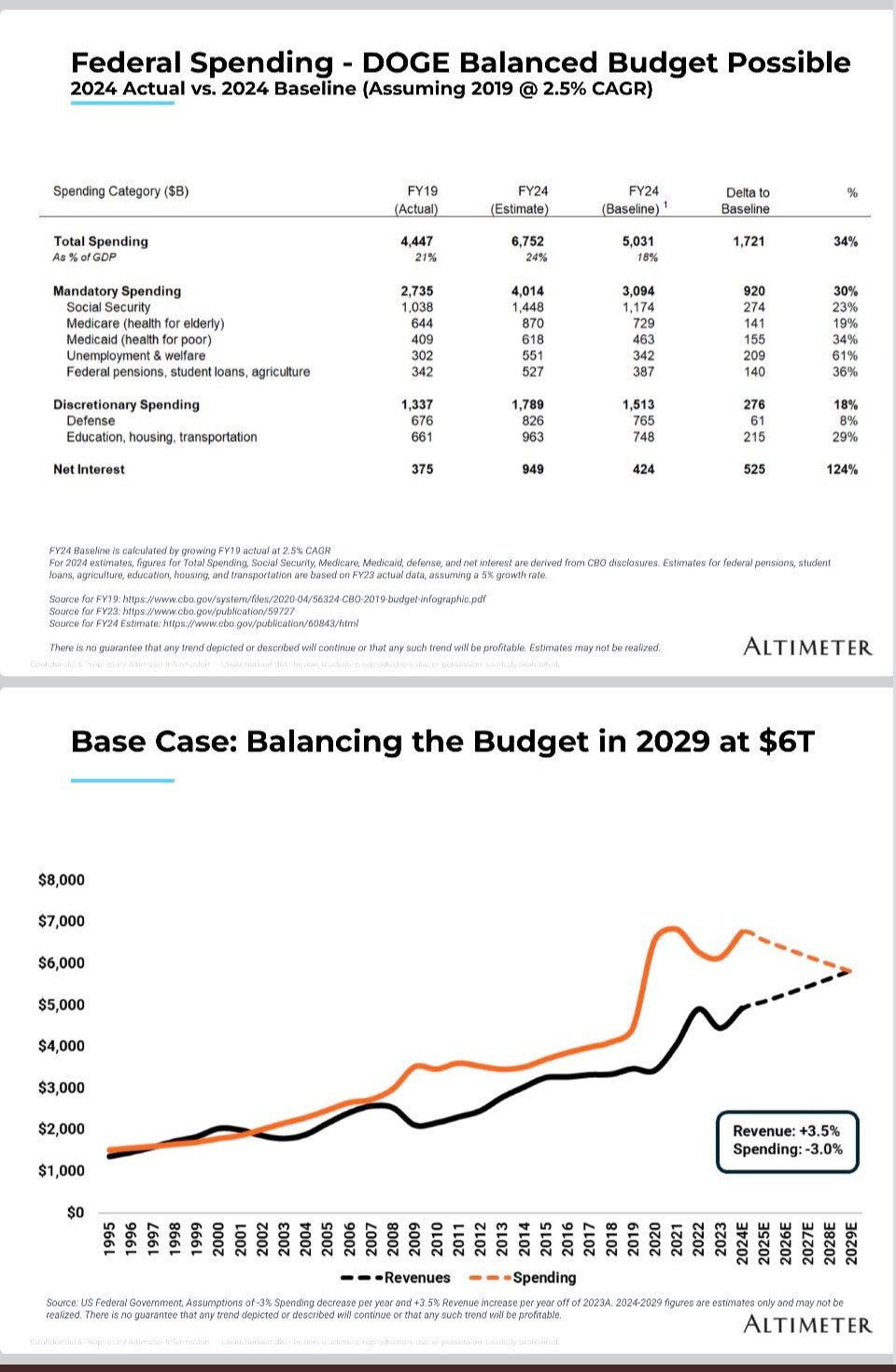

To start, all we may have to do is roll back spending to 2019 levels to get deficits under control, as some prominent investors have said. 2024 revenues are greater than 2019 spending levels.

Let’s go!👇

Heck, last year the federal government itself said there could be upwards of $500 billion/yr just in fraud, every year! Ahhhhhh.

Whatever it is, in order for rates to drop, we need a signal to the bond market to relax their grip. 10-yr treasury rates would then fall, as would mortgage spreads (the difference between the 10-year yield and the 30-year mortgage rate), further bringing down mortgage rates.

So is it possible to get spending under control enough to get mortgage rates down, to say, the 5.50%-5.99% range?

Yes!

But only time will tell. But I think there is a better chance than not that in 2025 we can get to 5-something % rates.

We just need our government leaders to get their shit together.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

P.S. Want to protect yourself from inflation? Buy a rental property; buy real estate. Don’t know how to get in or where to start? Give us a call! We got you.

Subscribe Today! (and get some amazing perks)

Paid subscribers get the best stuff! Join the Skeptical Investor Community to access:

Premium content and NO paywall,

Every article we have published - a treasure trove of information and education,

Conversations with other investors in the Skeptical Investor community, and future meetups and special events,

Key insights and predictions on the latest financial news,

PLUS, subscriptions include an annual one-on-one call with me personally. So make sure to take advantage! Subscribe today.

Just $5 bucks a month.👇

We have passed 10,000 subs! Thank you for your support, next stop, 20,000!

Please help grow the community!

It takes me several hours to write this weekly article, and they will always remain free (but you get some pretty cool perks with premium, including a one-on-one with yours truly :). All I ask is that you share it with 1 friend. Just 1. If you do, you will get two gifts: free education for one of your friends, and good karma for helping to grow a community of folks trying to figure out a way to create wealth for their family.

What, did you think I was going to send you a Starbucks gift card? 😅

Ready to Start Investing in Real Estate?

We are real estate agents for investors, because we are investors. We specialize in helping investors find, analyze and negotiate great real estate deals, as well as manage their rental properties, here in Nashville, TN. We pride ourselves on being tough negotiators. We want our clients to get an amazing deal, we never let our clients pay retail.

If you are looking for an investment property, give us a call today!

You can also find out more about us and what we offer on our website: www.NashvilleInvestorAgent.com

Why Nashville? There is always a bull market somewhere, and one of them is Nashville. We have the lowest unemployment rate of the top 25 major cities and folks are moving here to take those jobs. Nearly 90+ people per day move to Nashville. And tourism continues to hit record levels. This past year 16.8 million folks visited our lively city. Plus we have 3 professional sports teams (hopefully a 4th soon), massive healthcare and entertainment industries, heavy manufacturing, more than a dozen colleges, no state income tax… to name a few amazing advantages. Come check us out, the water is warm :).