Welcome to the Skeptical Investor Newsletter. A frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

The Weekly 3 in News:

73.3% of U.S. mortgage borrowers have an interest rate under 5.0% (Lambert).

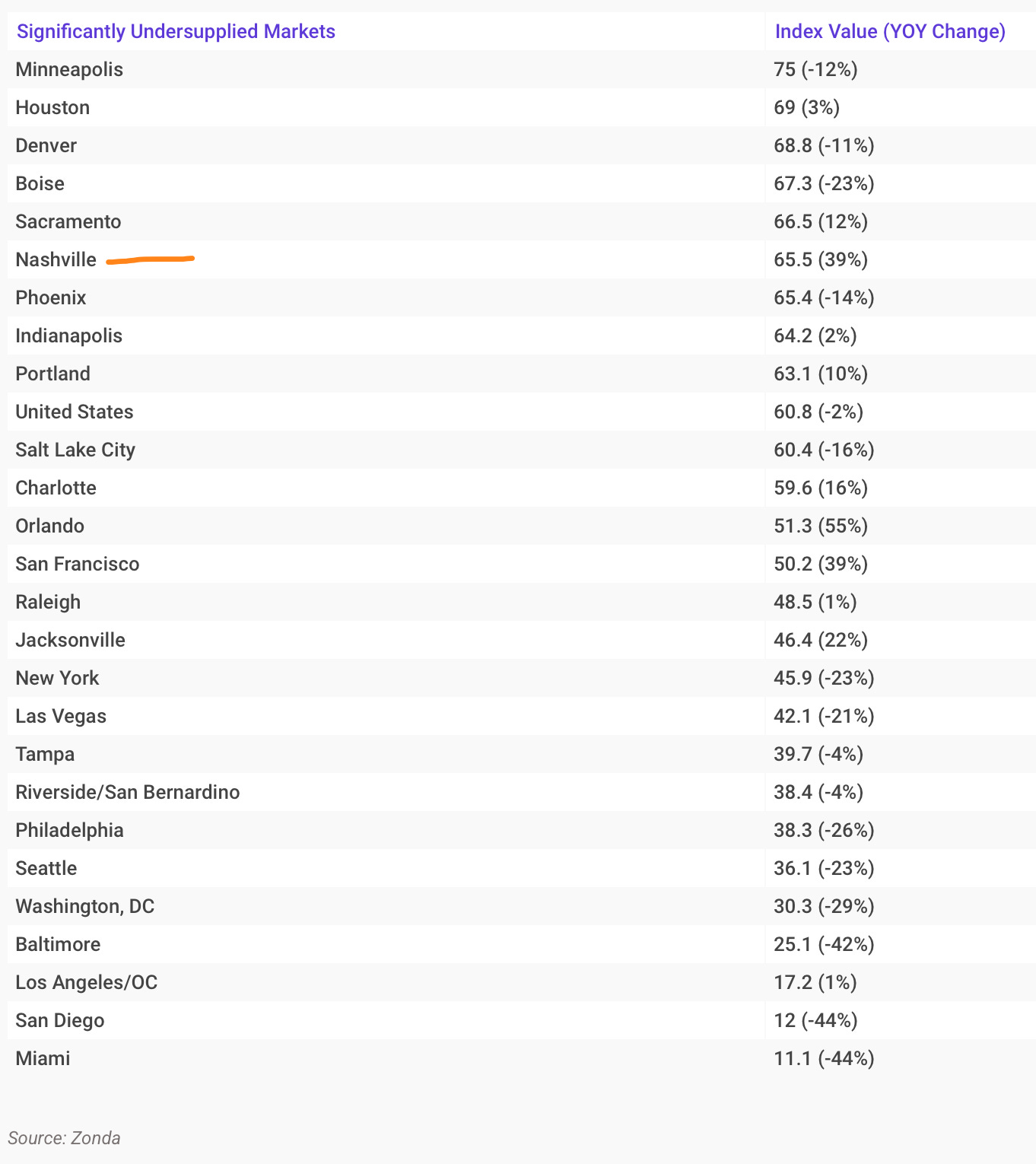

Most housing markets are significantly undersupplied for new lots to develop, including Nashville. We need more housing (Zonda)!

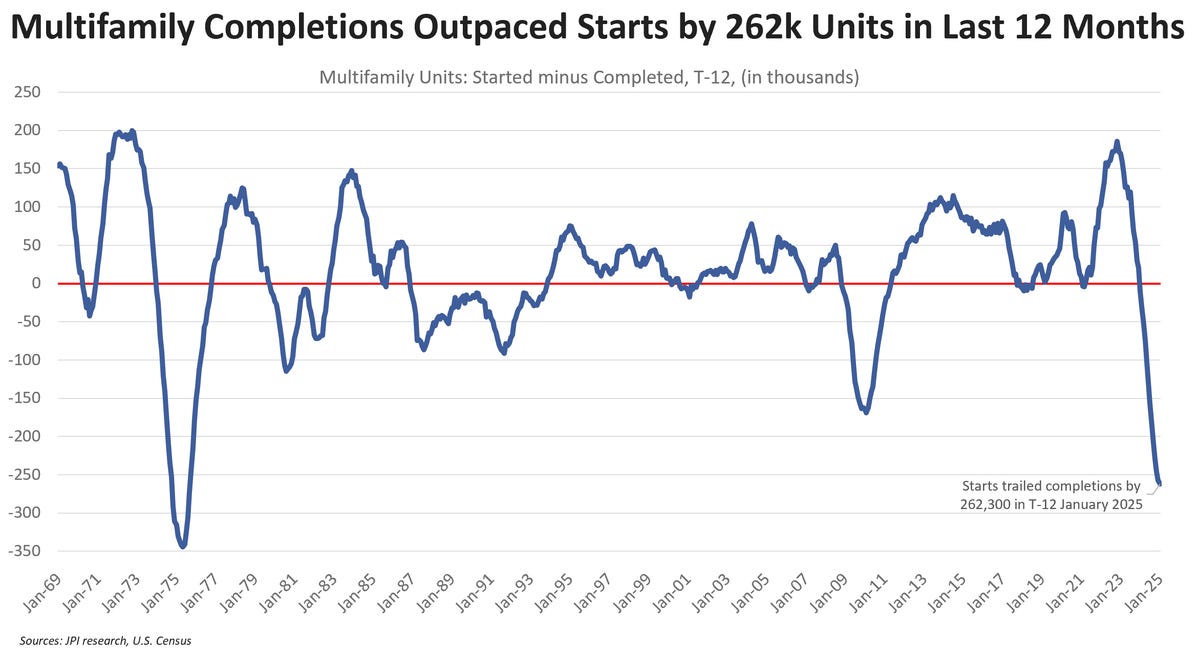

New apartment construction continues to plummet. Apartment development starts are trailing completions by the most since the 1970s. We are entering into a severely undersupplied housing moment as interest rates weigh on development (Parsons).

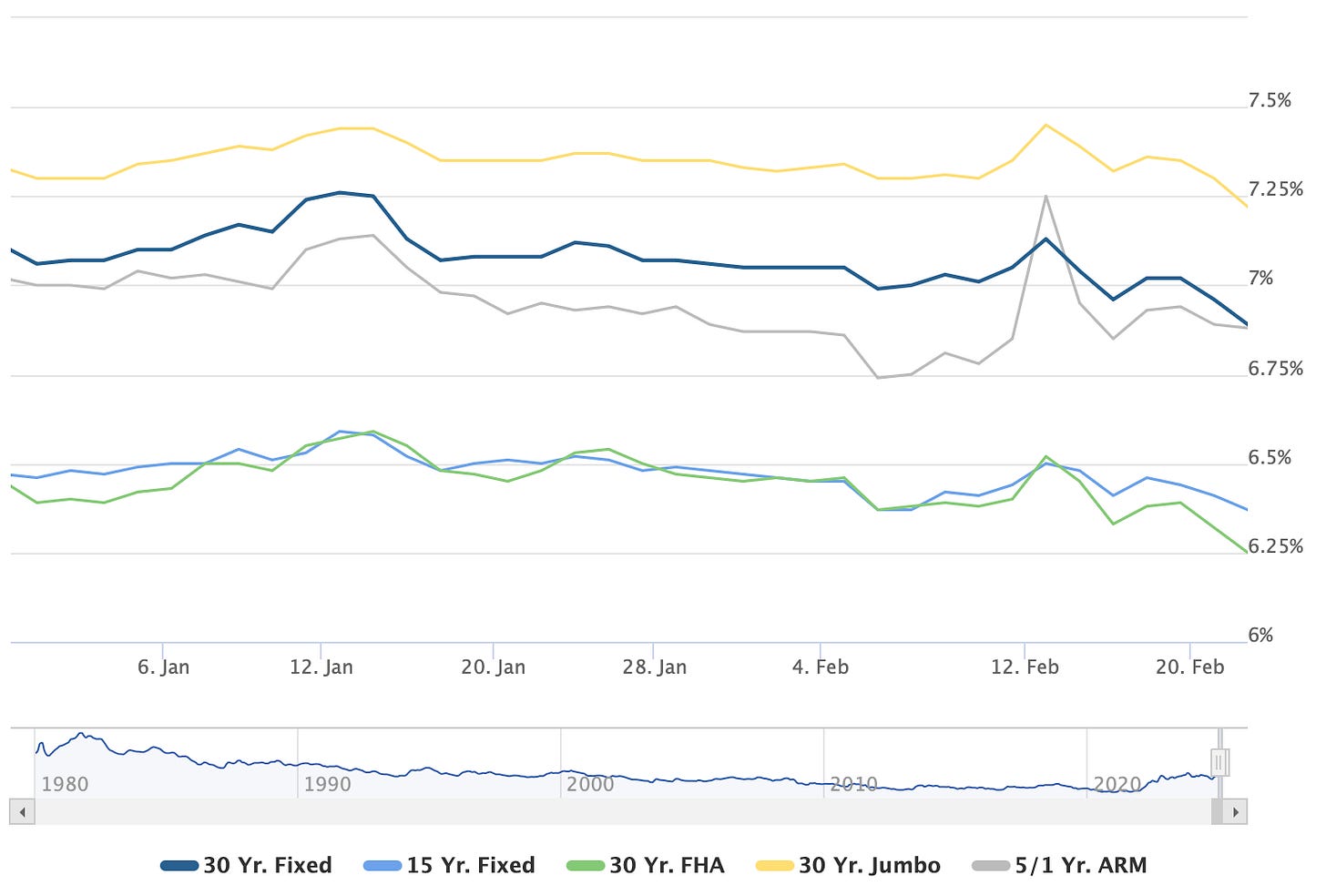

Today’s Interest Rate: 6.87%

(👇.09% from this time last week, 30-yr mortgage)

Today, we’re talkin’ markets, and where they go from here. Is inflation at risk of reigniting or is the long-term downward trend still intact? Will there be a catalyst for housing activity like lower interest rates? Or will rates continue to stay high?

I found some interesting countertrends this week.

Let’s get into it.

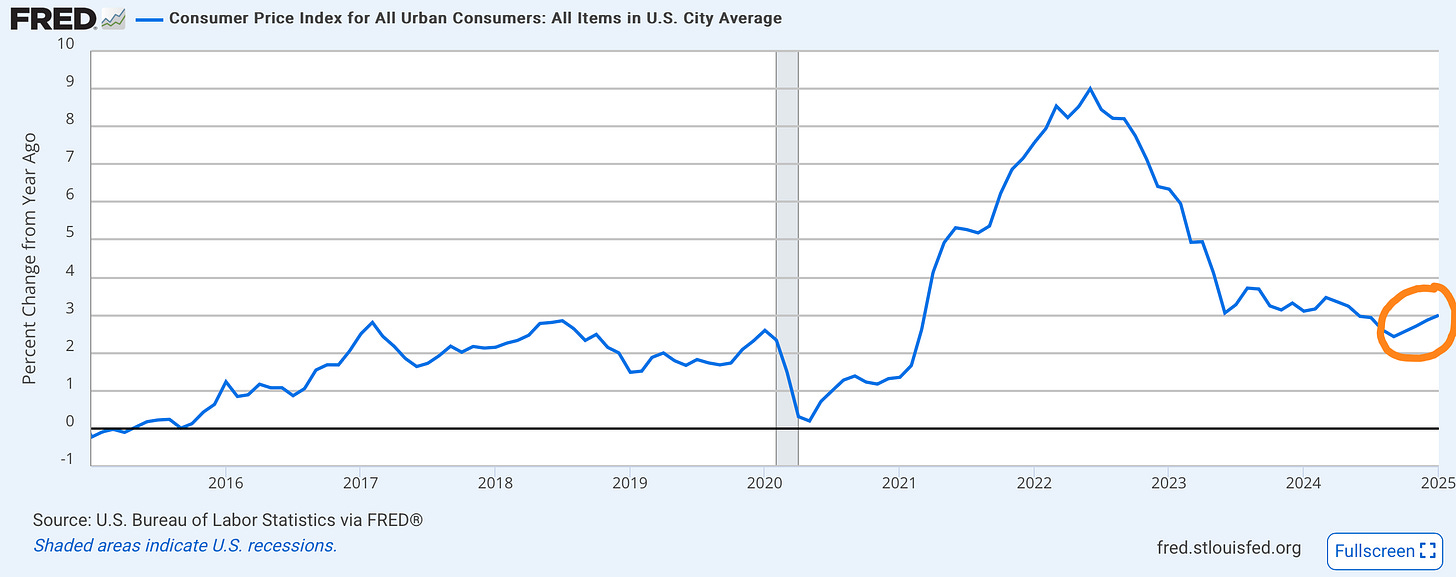

Inflation has been trending higher

Inflation has come down significantly since its peak. A few years ago prices were going up 9%, and now we have settled ~ 3% price growth. But this ain’t good enough, and is still 50% higher than the Fed’s 2% target.

And to his credit, Federal Reserve Chair Jerome Powell seems in no rush to cut rates with inflation above target level. During his congressional testimony last week, Powell said, “If the economy remains strong, and inflation does not continue to move sustainably toward 2 percent, we can maintain policy restraint for longer.” And that “the Fed would not lower its policy rate until there is “greater confidence that inflation is moving sustainably down toward 2 percent.” This is a welcome, cautious approach prioritizing inflation data over premature rate reductions.

However…. it appears that inflation may instead be reversing course.

It’s been four straight months of price increases.

October - 2.57%

November - 2.71%

December - 2.87%

January - 3%

Four, a trend does make.

And oddly, Fed Chair Powell seemingly brushed this off in his testimony, saying “A couple of months doesn’t make a trend.” This is not accurate. I couldn’t believe it.

This is a big deal, and it seems nobody is talking about it. A not so fun fact, we have not had more than 2 consecutive months of inflation growth since the end of 2021.

Until now.

I’m getting PTSD from when the Fed and former Treasury Secretary Yellen insisted for months and months that inflation was not a worry, it was “transitory..”

How did that play out y’all?

So count me extremely skeptical. Inflation has a real risk to the upside here.

Do you hate email? I do.

Well, they finally did it, an AI email assistant. Let AI do email for you. Read, filter, respond, notate, a back massage for crooked neck (ok not that, yet)…it’s Fryer AI.

Begin your day with emails neatly organized, replies crafted to match your tone, and crisp notes from every meeting….Holy hell they did it. It’s superhuman and frankly amazing! Links to your Gmail or other email service.

Plus, you get a free 7-day trial from us at the Skeptical Investor.

Support our pirate ship by clicking the ad below, each click promotes our newsletter! 👇

Sell Smarter with Fyxer AI

Fyxer is the AI Executive Assistant for busy property specialists:

Emails organized.

Personalized replies written in your tone.

Detailed notes from every meeting.

Less time on admin, more time on deals.

Where do interest rates go from here?

Now, here is where it starts to get interesting.

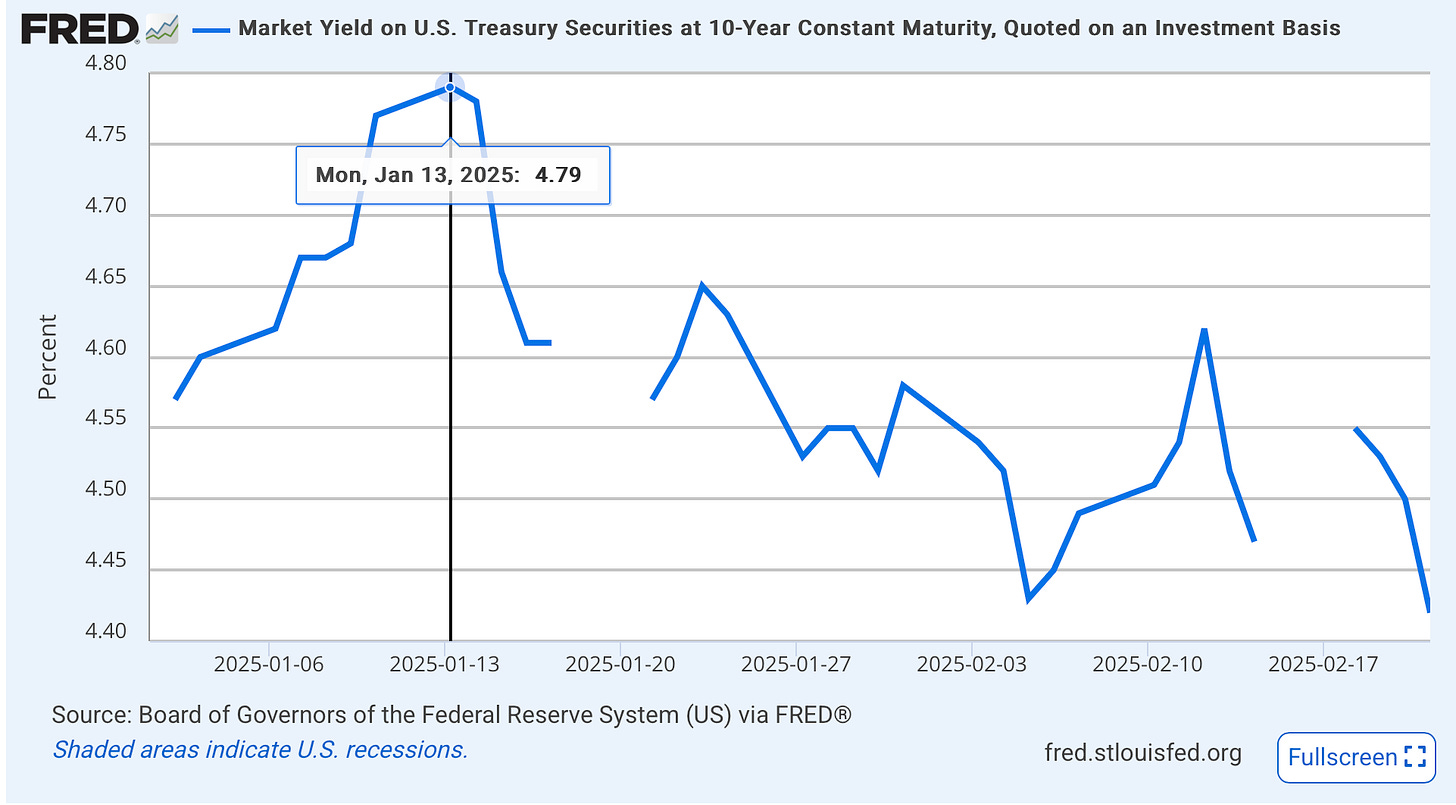

After having a bit of a tantrum to start the year, where the 10-yr treasury spiked to ~4.8%…

…bond vigilantes have been feeling better about inflation’s prospects these last few weeks (the breaks above are holidays).

This has translated into (slightly) lower mortgage rates.

Since peaking on Jan 13th (matching the 10-yr Treasury peak) at 7.26% the 30-yr mortgage rate has been down each week since (with some volatility last week).

Very interesting.

And, ironically, this could continue.

In an interview this past Friday, Treasury Secretary Bessent told Bloomberg that the Fed may stop selling Treasuries off their balance sheet, which the Fed has been doing while lowering interest rates. These two actions were working against each other, so if they do stop Treasures rolling off, this will make it easier (with lower supply) for the Treasury to issue/sell 10yr bonds and potentially lead to lower long-duration bond rates, and thus mortgage rates.

The Fed doesn’t control mortgage rates, but they do own mortgage bonds

It is often said, including by yours truly, that the Fed doesn’t control the long end of the yield curve. Ie, when the Fed cuts it’s short-term Fed Funds Rate that does not have a direct affect on 10-yr Treasury rates, or 30-yr mortgage rates.

True. But…

Consider Becoming a Paid Subscriber!

The Skeptical Investor Newsletter is just the beginning, consider becoming a paid subscriber. Get premium content and live 1-on-1 calls with yours truly. Just $5 / mo. Let’s chart a path for your next real estate investment today.

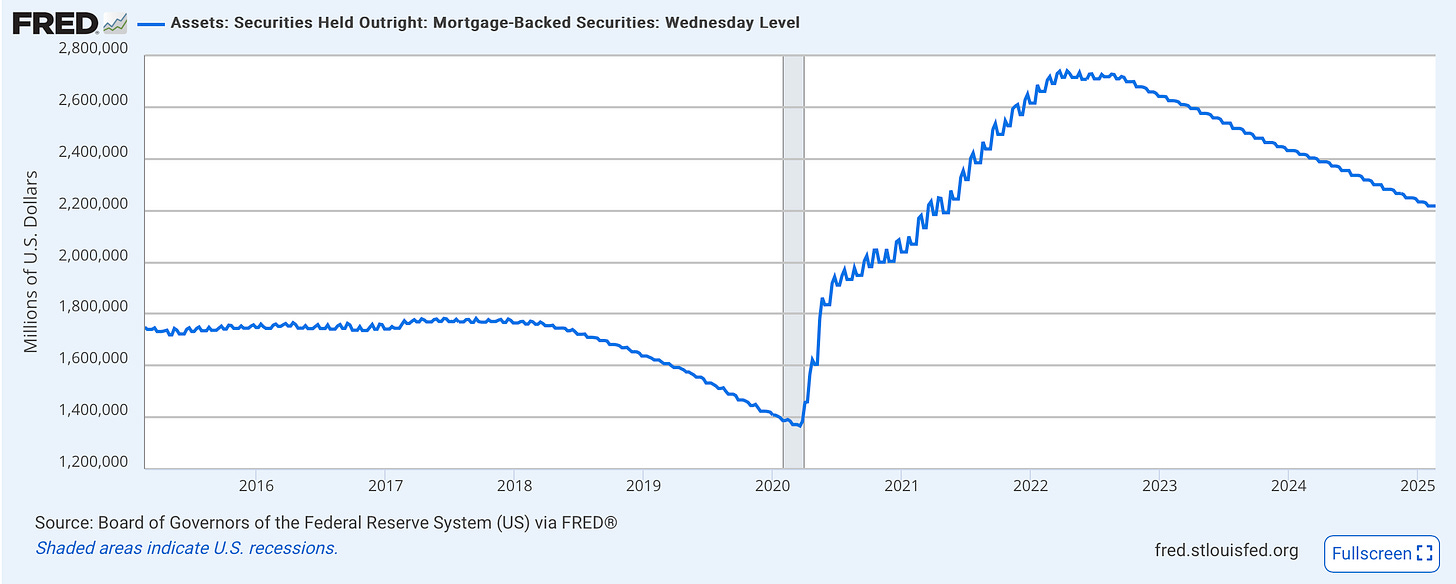

The Fed does buy mortgage bonds (mortgage-backed securities). Currently $2.2 trillion worth, in fact. This is called Quantitative Easing (QE) and it very much affects interest rates. Treasury bonds are long-term debt securities issued by the government to finance its spending. When the central bank engages in QE and buys treasury bonds, it increases the demand for these bonds. Higher demand for treasury bonds leads to an increase in their prices. Bond prices and yields are inversely related: when bond prices rise, yields fall. Therefore, QE lowers treasury bond yields. And since the 30-yr mortgage follows the 10-yr Treasury rate (put simply: they are competing investment tools) the Fed very much can affect mortgage rates.

This QE mortgage rate manipulation became a policy tool in 2009, following the Great Financial Crisis. And it will remain so, until the Fed mortgage bond portfolio drops to zero. So when the Fed buys mortgage bonds they can manipulate mortgage rates down by introducing additional demand. This contributes to a higher-than-usual premium in the spread between the 10-year Treasury and 30-yr mortgage rates i.e. higher mortgage rates.

The complication today is that since buying a hell of a lot of these bonds from 2020-2022 they have been steadily selling them back into the market or allowing them to roll off/expire.

This does put upward pressure on mortgage rates.

The Market Lives in the Future

Beyond directly lowering treasury yields, QE increases the overall money supply in the economy. This influx of money can lead to lower interest rates across various financial markets, including mortgage rates. The signaling effect of QE also plays a role. When the central bank engages in QE, it signals its commitment to keeping interest rates low for an extended period. This influences market expectations and reinforces the downward pressure on mortgage rates.

Labor market softening could further help with rates

In his testimony, Powell also remarked that the labor market has "cooled from its formerly overheated state" but remains "solid." He continued, saying “[the Fed can] "ease policy if the labor market unexpectedly weakens or inflation falls more quickly than expected." This shows that the Fed is prepared to lower interest rates if the job market suddenly deteriorates or if inflation drops faster than anticipated.

Welcome reassurance to the market.

Additionally, Powell noted that the Fed is in the midst of a framework review, evaluating its monetary policy and communication strategies. This should wrap up by late summer 2025 and could provide a pivot point for Fed policy.

My Skeptical Take:

The 4-month inflationary trend should be extremely concerning. I am skeptical that the Fed will be able to cut rates by the conclusion of its framework review this late summer.

Last month I made a call on mortgage rates for 2025.

And I’m sticking by it.

So, if the Fed won’t do it, how could mortgage rates drop?

I still think we can get to sub-6% this year on the 30-yr mortgage. But it won’t be because of the Fed cutting rates. It will be because these 3 things happen:

The labor market continues to normalize (aka cool), wage inflation slows but not alarmingly, and the bond market can stop fighting the Fed. Once bond market vigilantes believe that future inflation is under control, interest rates - and thus mortgage rates - will tick down (Long-term bonds will be more valuable and investors will buy them). Mortgage rates go down with Treasuries.

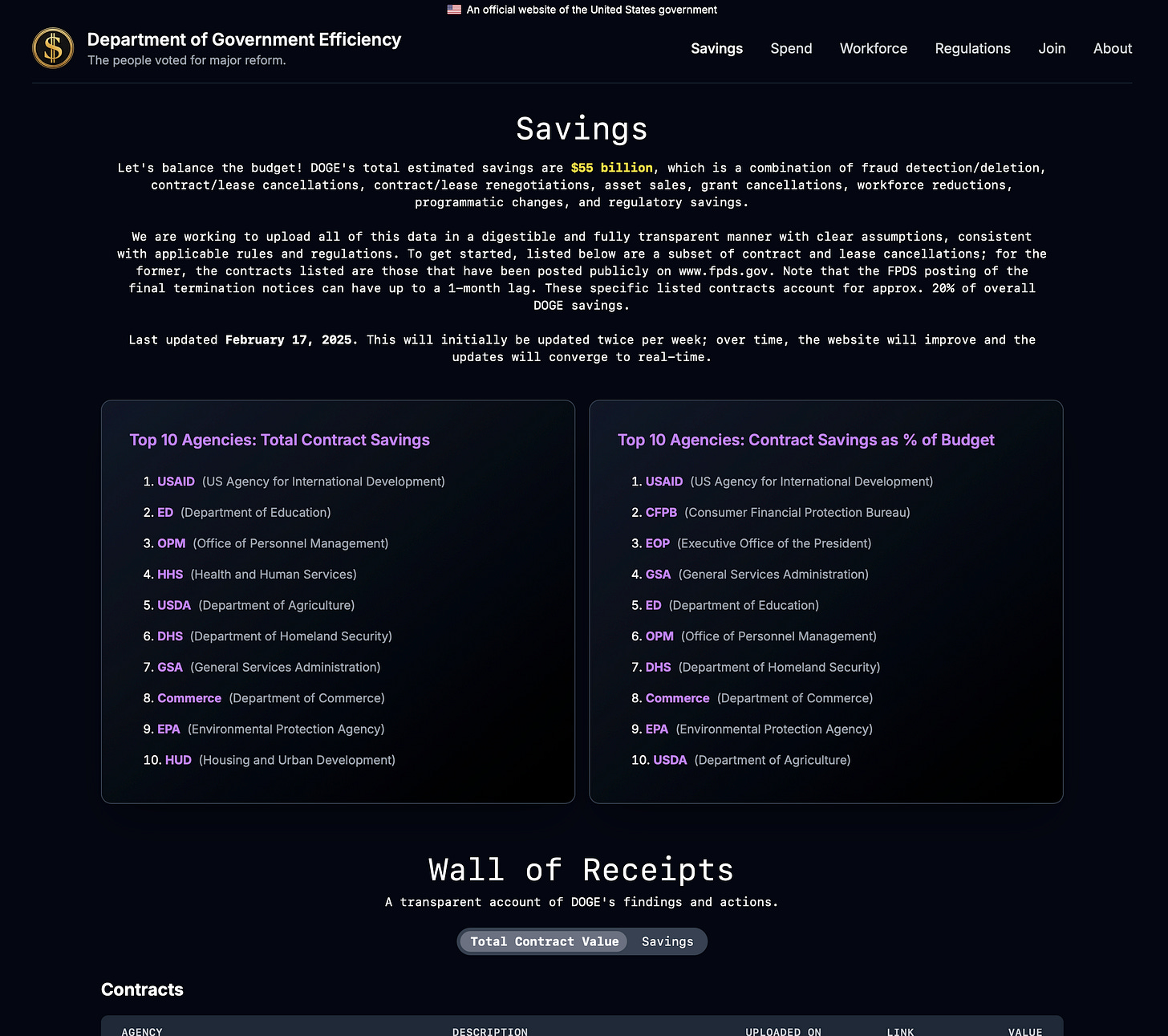

Government spending is being slashed (hopefully). If it becomes clear that the DOGE White House effort is working, long-term Treasury bill yields will fall even faster. Hell, DOGE says they have saved $55 billion in taxpayer dollars so far, according to the Administration’s new “transparency” website. This may be “inflated” (pardon the pun) and the effort has received criticism BUT if they can achieve even a fraction of the $2 trillion they intend to cut it will be enough of a signal.

Remember, it’s been just 30 days since they started.

The Fed can use its balance sheet to affect mortgage rates. The Fed doesn’t need to start buying mortgage bonds again (ie quantitative easing) but it can stop selling/rolling mortgage bonds off its balance sheet. It has $2.2 trillion of these babies and continuing to release them back into the market is likely putting upward pressure on rates. And if the housing market stays in correction territory (by # of transactions) then they may even consider adding to their treasure trove of Treasuries (say that 5 times fast).

So, will we get to 5.xx% mortgage rates this year?

Yes we can.

All the market needs is confidence that inflation and federal spending are starting to tick down, with a cool, yet steady, labor market.

Remember, the market lives in the future.

I’m not assuming anything of course. And I recommend you do the same.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

P.S. Want to protect yourself from inflation? Buy a rental property, buy real estate. Don’t know where to start? Give us a call! We got you.

Subscribe Today! (and get some amazing perks)

Paid subscribers get the best stuff! Join the Skeptical Investor Community to access:

Premium content and NO paywall,

Every article we have published - a treasure trove of information and education,

Conversations with other investors in the Skeptical Investor community, and future meetups and special events,

Key insights and predictions on the latest financial news,

PLUS, subscriptions include an annual one-on-one call with me personally. So make sure to take advantage! Subscribe today.

Just $5 bucks a month.👇

We have passed 10,000 subs! Thank you for your support, next stop, 20,000!

Please help grow the community!

It takes me several hours to write this weekly article, and they will always remain free (but you get some pretty cool perks with premium, including a one-on-one with yours truly :). All I ask is that you share it with 1 friend. Just 1. If you do, you will get two gifts: free education for one of your friends, and good karma for helping to grow a community of folks trying to figure out a way to create wealth for their family.

What, did you think I was going to send you a Starbucks gift card? 😅

Ready to Start Investing in Real Estate?

We are real estate agents for investors, because we are investors. We specialize in helping investors find, analyze and negotiate great real estate deals, as well as manage their rental properties, here in Nashville, TN. We pride ourselves on being tough negotiators. We want our clients to get an amazing deal, we never let our clients pay retail.

If you are looking for an investment property, give us a call today!

You can also find out more about us and what we offer on our website: www.NashvilleInvestorAgent.com

Why Nashville? There is always a bull market somewhere, and one of them is Nashville. We have the lowest unemployment rate of the top 25 major cities and folks are moving here to take those jobs. Nearly 90+ people per day move to Nashville. And tourism continues to hit record levels. This past year 16.8 million folks visited our lively city. Plus we have 3 professional sports teams (hopefully a 4th soon), massive healthcare and entertainment industries, heavy manufacturing, more than a dozen colleges, no state income tax… to name a few amazing advantages. Come check us out, the water is warm :).