Welcome to the Investor Agent Real Estate Newsletter. A frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

Today We’re Talkin:

The Weekly 3 - News, Data and Education.

What the ‘H-E-Double Hockey Sticks’ is up with Mortgages?

Is a Return to Inflation a Real Risk?

Cautious Skepticism on Rate Cuts

Real Estate Activity Update

My Skeptical Take.

The Weekly 3: News, Data & Education

Housing Supply Success Stories - “No single legislative action did more to contribute to housing creation than the elimination of parking minimums [in Minneapolis].” This is how you help solve the housing shortage. Allow more buildings per sq ft. We don’t need more money, just smart policy (Austin, TX did something similar as well). (Lind).

US GDP Growth in 2023 was 2.5%, almost exactly the long-term average. This, despite politicals calling it the best economic in decades. (BEA).

The Era of Abundant Energy May Be Coming. Microsoft plans to reopen Three Mile Island nuclear plant, while Amazon has invested in a data center campus powered by one of the largest existing nuclear facilities in the US. Why? We can now “compress energy into intelligence” through A.I. ~ Jensen Huang (Chmath).

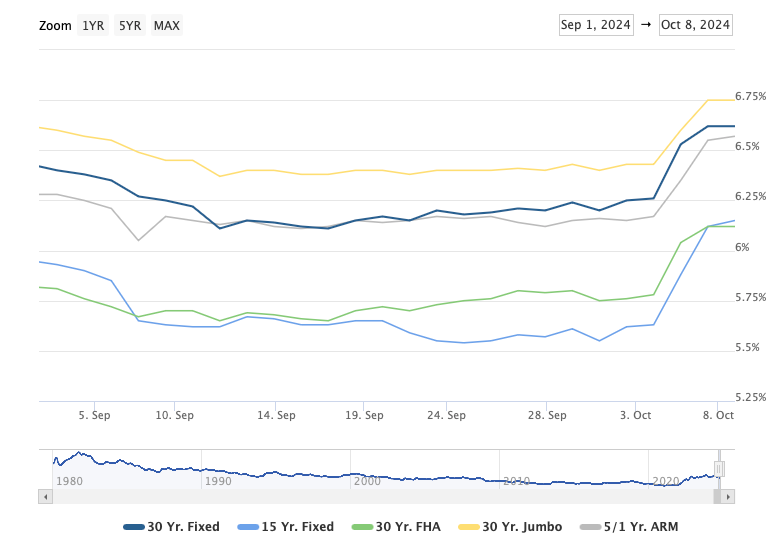

Today’s Interest Rate: 6.62%

(☝️.37, from this time last week, 30-yr mortgage)

Guten Morgan investors. It’s a lovely day to talk real estate. Let’s get into it.

What the ‘H-E-Double Hockey Sticks’ is up with Mortgages?

Well, we said this may happen, the Fed announced an interest rate cut, and even though it was a larger cut than we expected (.5%), the bond market reacted in reverse, Spiking mortgage rates up.

Mortgage rates are up nearly .5% since the Fed cut rates.

Mortgage Rates

We wrote about this 2 weeks ago and expected this reaction, but I must admit I am a little surprised at the degree of uptick. It hasn’t been volatile; it’s been lower left → upper right this last week.

The Fed Can’t ‘Fix’ the Housing Market

As a reminder, the Fed does not control mortgage rates.

Mortgages are predominantly influenced by the market demand for 10-year Treasury bonds, not the Federal Reserve's adjustments to its short-term Fed-Funds rate. The 10yr and 30yr mortgage are competing assets investors buy in the market, expecting a return for their expected risk. If investors expect higher risk to the economy, they buy 10-yr Treasuries, if the future seems less risky, they buy 30-yr mortgages. Investors also sell Treasuries if they see inflation on the horizon, which would erode their returns (yes yes, this is all oversimplified, hold your comments angry-web).

The Fed can’t alone ‘fix’ the housing market but it can assist with cheaper debt (ie interest rates). Last month Fed Chair Powell made some salient points, saying:

“The housing market, it’s hard to game that out. The housing market is, in part, frozen because of lock-in, lower rates, people don’t want to sell their home because they have a very low mortgage and it would be quite expensive to refinance. As rates come down, people will start to move more and that is probably beginning to happen already. But remember, when that happens you’ve got a seller but you also got a new buyer in many cases. So it is not obvious how much additional demand that would make. The real issue with housing is that we have had, and are on track to continue to have, not enough housing. And so it’s going to be challenging, it’s hard to zone lots in places people want to live. All of the aspects of housing are far more difficult, and where are we going to get the supply? And this is not something the Fed can really fix. But as we normalize rates, I think you’ll see the housing market normalize. Ultimately by getting inflation broadly down and rates normalized and getting the housing cycle normalized, that is the best thing we can do for householders. And the supply question will have to be dealt with by the market, and also by the government.” ~ Fed Chair Powell 9/18/24

So remember, a reduction in the federal funds rate does not directly or immediately impact housing prices or mortgage rates.

But they do rhyme.

For the last 7-30 days, we have been in a period of divergence. Fed Funds rate is down and mortgage rates are up.

Bond Market is Driving the Ship

It appears that the bond market doesn’t believe the Fed when they say that inflation is on the approach to land near their 2% target and / or they will be cutting rates much more slowly than they say. 10-yr treasuries have sold off, driving the yield up .4% just in the last week to 4.031%. Mortgage rates are 6.62%, a spread of 2.589%. (If spreads were at historical levels (1.74%) we would be at 5.77% 30-yr mortgage rates today.

Higher spreads indicate market nervousness.

Is a Return to Inflation a Real Risk?

In short, yes. The Fed needs to be careful over the next 12 months.

There are several non-structural reasons for the activity in mortgage rates, and it’s not just the bond market that is wreaking havoc on mortgage rates. Rates had already fallen 2% since the 8% high in Q4 2023. And had fallen sharply into the Fed’s September rate cut. This momentum downward likely caused a pullback on the news of a Fed cut, a natural part of a healthy market.

Additionally, last week, and to begin this week, there was rapid movement upward resulting from a positive jobs report that was ‘hotter’ than expected. U.S. employers added 254,000 jobs last month and unemployment ticked down a titch to 4.1%, the Labor Department said Friday.

Economists expected payrolls to increase by 150,000 in September, and the unemployment rate to hold at 4.2%. Well… you know what they say about economists…(keep reading 🤥 ).

Jobs = Good, No?

Now most folks would think: “yay, more jobs!,” but the market interpreted that as a potential return to inflation or an extended timeline for the Fed to cut rates. After all, why cut rates quickly if the economy is booming and jobs are plentiful? This is driving a sale in 10yr treasuries.

We are in a tumultuous time so good economic news is bad for debt markets. I know…. crazy upside down town.

Cautious Skepticism on Rate Cuts

Comments by former Treasury Secretary Larry Summers - one of the ‘good’ economists out there - echos this sentiment. He sees the Fed as taking the cautious/slow approach to rate cuts, even going so far as to say the larger .5% cut was a “mistake,” while pointing out that wage growth is strong, above 2019 levels, which could risk inflation returning.

So What’s Next for Rates?

My prediction is still for mortgage rates to hit 5.5% in 2025, likely in the Spring, maybe summer timeframe. I am more bullish on lower rates than most investment banks / economists, many of whom are calling for ~5.9% by Q4 2025. I do think, in hindsight, we will see that the economy is presently in a 12-month cooling cycle and this momentary uptick will be relatively fleeting and caused by normal debt market activity.

Real Estate Activity Update

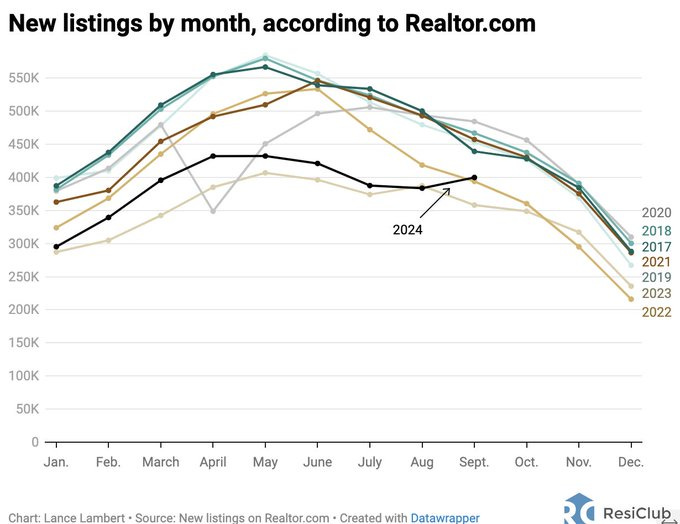

New listings are higher in the short-term but remain historically depressed, like a drizzly day in Seattle. Folks like their low-rate mortgages aren’t yet ready to sell, only to have to buy again. New homes are still making up a larger % of home sales because of this “lock-in effect.”

@NewsLambert

And September sales numbers YoY were up, but below historical levels.

@NewsLambert

Skipping Till Spring

Again, I think folks take the fall/winter off, and go do something else with their lives besides real estate (I know, how could someone do that)?! And returns in the Spring, ready to pounce (keep reading).

My Skeptical Take:

I remain skeptical that the Fed can pull off a “soft-landing. Especially one that is without a little drama. We’ll get there (neutral Fed policy, and calm jobs, unemployment and inflation numbers), but the ride is what we care about for these next 6 months or so.

Economists never get this right. Fun fact, the Fed has 400 Ph.D. economists, 500 researchers and 23,000 employees.Ok, two questions:

Why? (That’s a lot of people/experts).

How’s that going?

So what do they say about economists? I’ll let Nassim Taleb tell you, in the style that only he can:

An economist is a mixture of 1) a businessman without common sense, 2) a physicist without a brain, and 3) a speculator without balls.

Sick burn Nassim.

Getting this election and news media insanity past us will help too. I can’t wait for my email inbox, random phone calls, Twitter feed and friends and family to all go back to Dr. Jeckel; Mr. Hyde sucks.

Homebuyers Skip Till Spring, But Investors are Looking Now

All signals are pointing to a hot n’ sexy Spring housing season, fueled by a strong enough economy, good vibes post-election and lower Spring mortgage rates.

Until then, investors have a ~5 month window to buy properties before the hoard of homebuying orks stampedes in. Fewer buyers in the arena and increased housing inventory on the market is a perfect cocktail to pick up a deal.

December is my favorite month for big game hunting. Get out there.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

It takes several hours to write this weekly article, and they will always remain free. All I ask is that you share it with 1 friend. Just 1. If you do, you will get two gifts: free education for one of your friends, and good karma for helping to grow a community of folks trying to figure out a way to create wealth for their family.

What, did you think I was going to send you a gift card? 😅

Invest in Nashville Real Estate!

If you are interested in talking real estate investing and digging deeper into any of these ideas don’t hesitate to reach out! I always like a rigorous discussion and helping fellow real estate investors.

Looking for a market to invest in? There is always a bull market somewhere, and one of them is Nashville, where we are seeing record tourism this year. And we had 16.8 million folks visit Nashville in 2023! 90+ people per day move to Nashville; yet, our city population is still under 700k. We have 3 professional sports teams (hopefully a 4th soon), massive healthcare and entertainment industries, heavy manufacturing, more than a dozen colleges, and no state income tax, to name a few. We have everything but the Ocean (although the lakes and rivers are plentiful).

Looking for a realtor in the Nashville area? We are Real Estate Agents for investors, because we are investors.We specialize in helping investors find great properties in Tennessee. Give us a call today!

* I write this myself and get it out for you all on the same day. Apologize in advance for the likely errata. Don’t have a team of editors, yet.

** The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and do not constitute financial advice.